Deferred expenses and prepayments¶

Prepaid expenses are very common in a company, usually due to the creditor’s requirements. It is common to have to pay, for example, a credit policy in advance, a lease, or an advertising campaign. We are referring to services that we pay for in advance and that will not be received until the following fiscal year or years.

A prepaid expense can be understood as one where the payment is made before acquiring the product or receiving the service. From an accounting perspective, prepaid expenses are those that are recorded in one fiscal year but actually correspond to a later period.

The simplest and most frequently used example is the payment of insurance. Insurance, logically, must be paid in advance and generally covers risks for a year. If we pay for the insurance in April of year 01 , we will have coverage until April of year 02. The payment was made in year 01, but it is not fair to allocate all the expenses to that year since part of the payment will benefit the following year. The portion of the expense that has already been paid but corresponds to the following year is considered a deferred expense.

For example, if our company pays for an advertising campaign in January that runs until June of the same year, the expense is recorded in the (627) Advertising account at the present moment. The payment is made in the current fiscal year, and there is no need to consider it as a prepaid expense since it does not span two fiscal years.

If we contract the campaign in September and it runs until March of the following year, part of the expense recorded in the (627) Advertising account does not correspond to the current fiscal year. This portion is what we consider a prepaid expense, and it will be recorded in the (480) account.

Note

The server checks once a day if an entry must be posted. It might then take up to 24 hours before you see a change from draft to posted.

Creating Periodic Accrual Entries¶

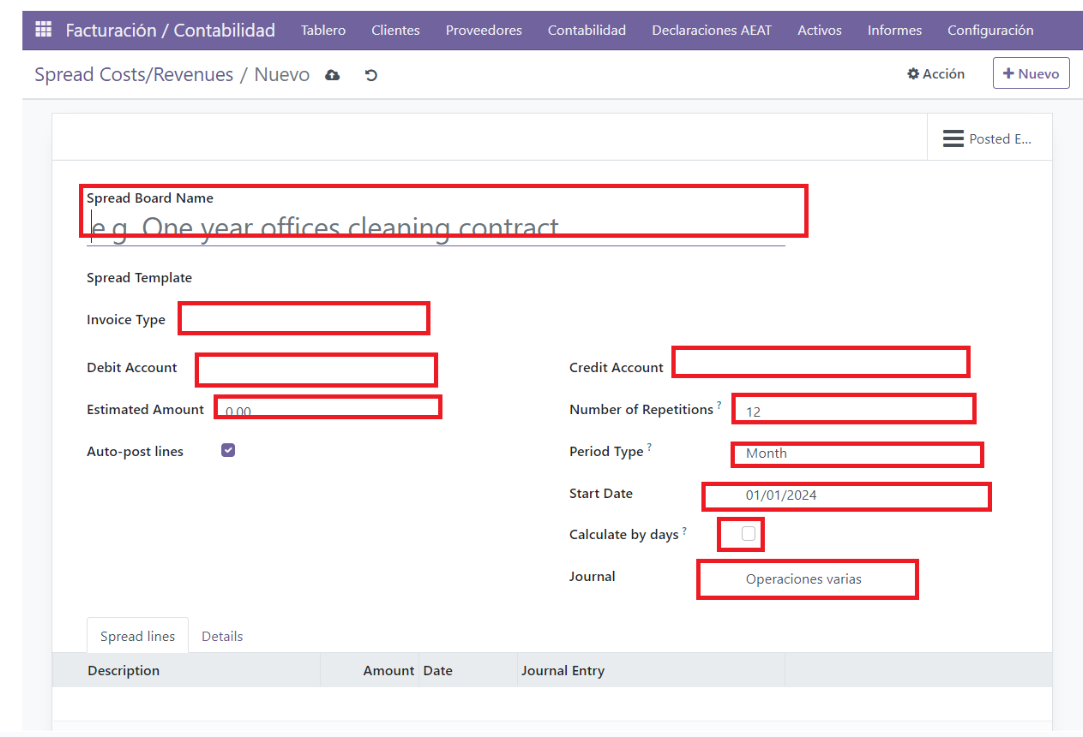

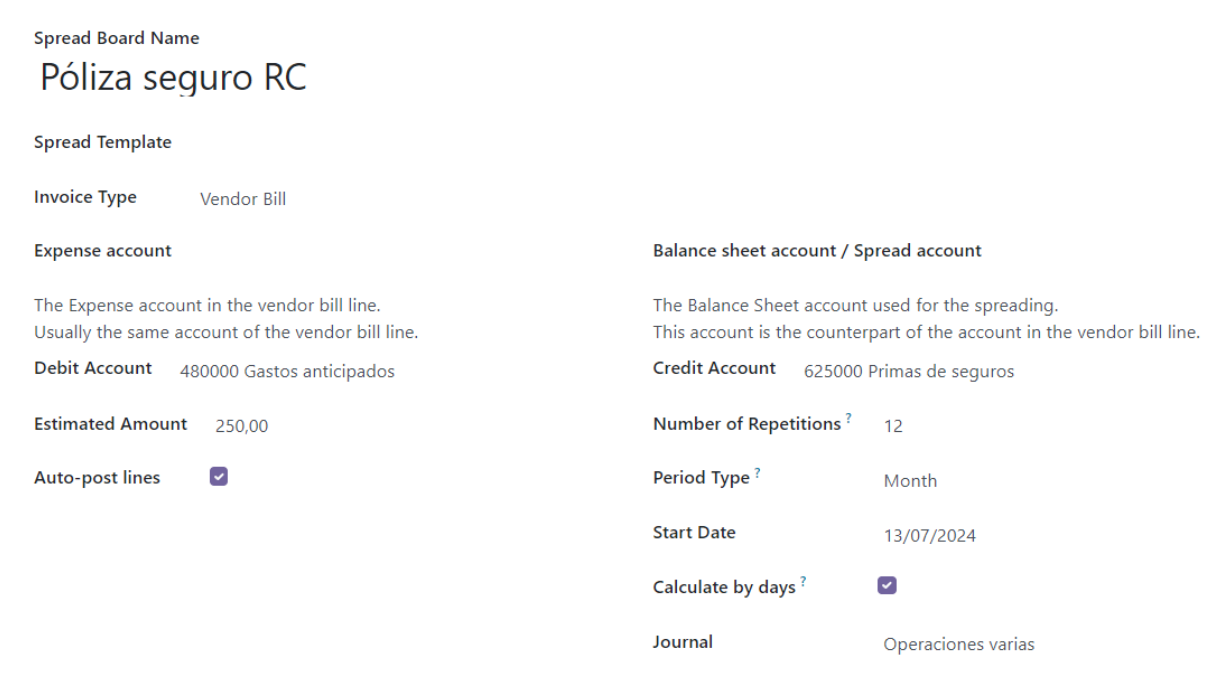

We must keep in mind that accounting for prepaid expenses and revenues is driven by the need to comply with the accrual principle. It is important to record the expense in advance, for example, the payment of insurance. Once recorded, we go to Accounting ‣ Spread Cost/Revenues ‣ New.

Expense Name: to identify the type of expense to be accrued.

Invoice Type: whether it is an expense or income.

Debit Account.

Estimated Amount: amount of the expense or income.

Credit Account.

Number of repetitions.

Period type.

Date the accrual begins.

Calculate by days.

Journal where it will be recorded.

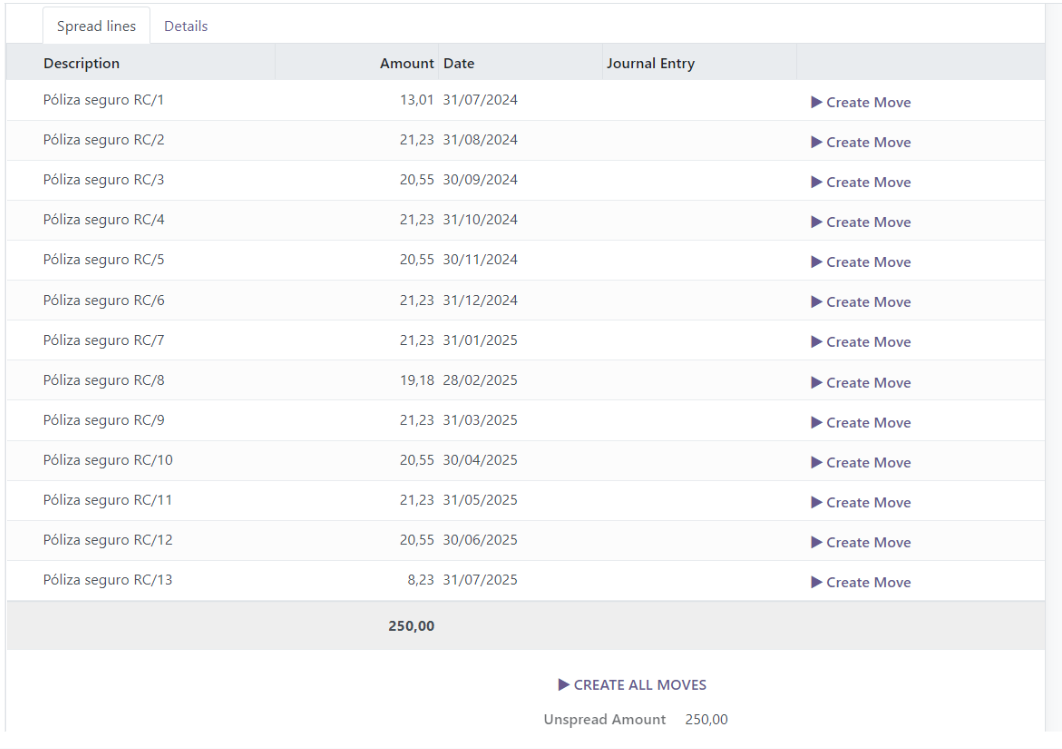

Once we have filled in the details, we press “Calculate.”

This way, the entry will be automatically calculated, and by pressing “Create Entry,” the accrual entry will be generated. Otherwise, it will remain as a draft. We can also press “Create All Entries” directly.